Do Developers Offer the Best Exposure to a Recovering Residential Market?

PUBLISHED

2023-06-13

Content

In our view, most commentary and solutions tend to miss the mark. While this article doesn’t attempt to address these issues, it raises another interesting topic. If house prices boomed over the past 20 years to the point of making ownership and renting unaffordable, then surely the residential development industry made a fortune? Further, if house prices are turning up again, then is owning residential developers the best way to access the upside to future house price gains?

The disconnect between developing and owning

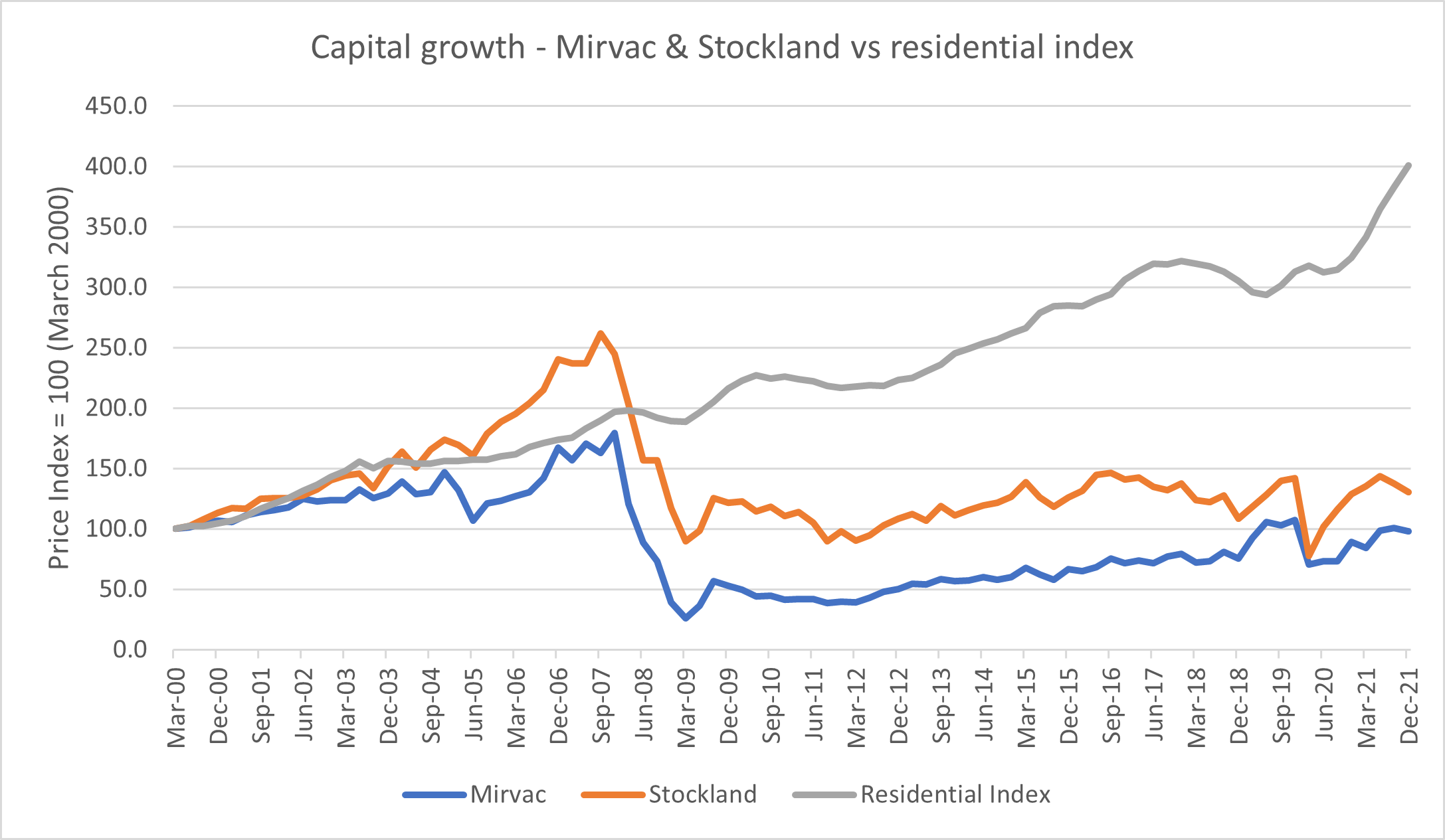

When assessing the share price performance of two of Australia’s largest listed residential developers (Mirvac and Stockland) over the past two decades, it’s clear that the ownership of the end product has been significantly more profitable than owning the manufacturer of the very same product. This reality runs counter to the popular ‘property is a bubble’ narrative that usually accompanies these types of discussions.

Source: Bloomberg, Quay Global Investors, ABS House price series

Now to be clear, we’re not trying to ‘pick on’ Stockland and Mirvac. It’s just that both companies have been listed for some time (lots of public information) and their business models are slightly different (Stockland on land banking and development, Mirvac on apartments development and communities).

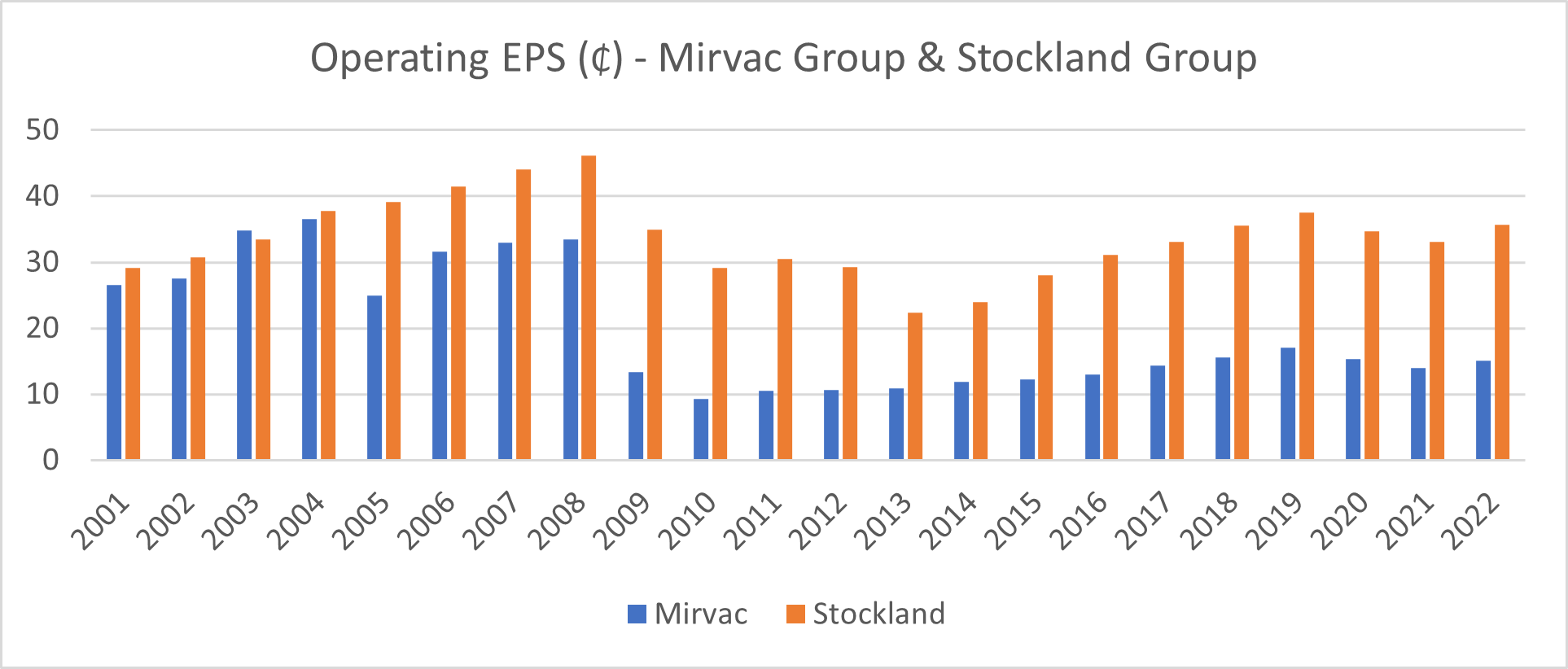

The disappointing long-term share price performance of these companies simply reflects the underlying operating earnings per share[1]. The lesson is that there has been very little economic gain being a ‘manufacturer’ of either developed land, residential communities or apartments in Australia for the past 20 years – despite the surge in property prices.

Source: Company annual reports, Quay Global Investors

Peeling back the diversified model

Mirvac and Stockland are not ‘pure play’ residential developers. They both have diversified operating models that include commercial real estate development and ownership (office, retail, industrial etc), hotel ownership and management, retirement, and funds management. Further, the dilutive effect of emergency equity issues during the GFC blur the line between long-term per share performance (earnings and price) and the underlying profitability of the development business.

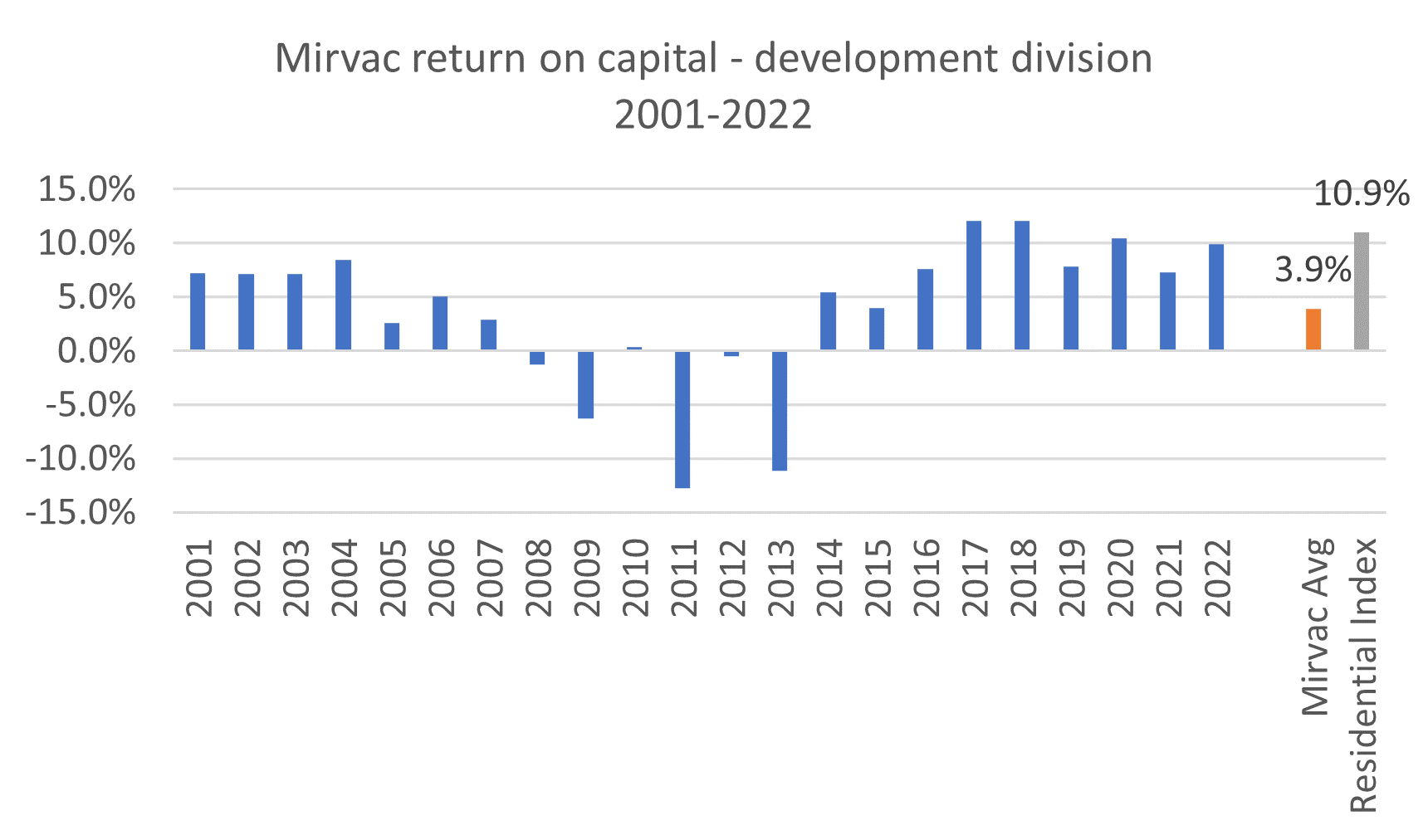

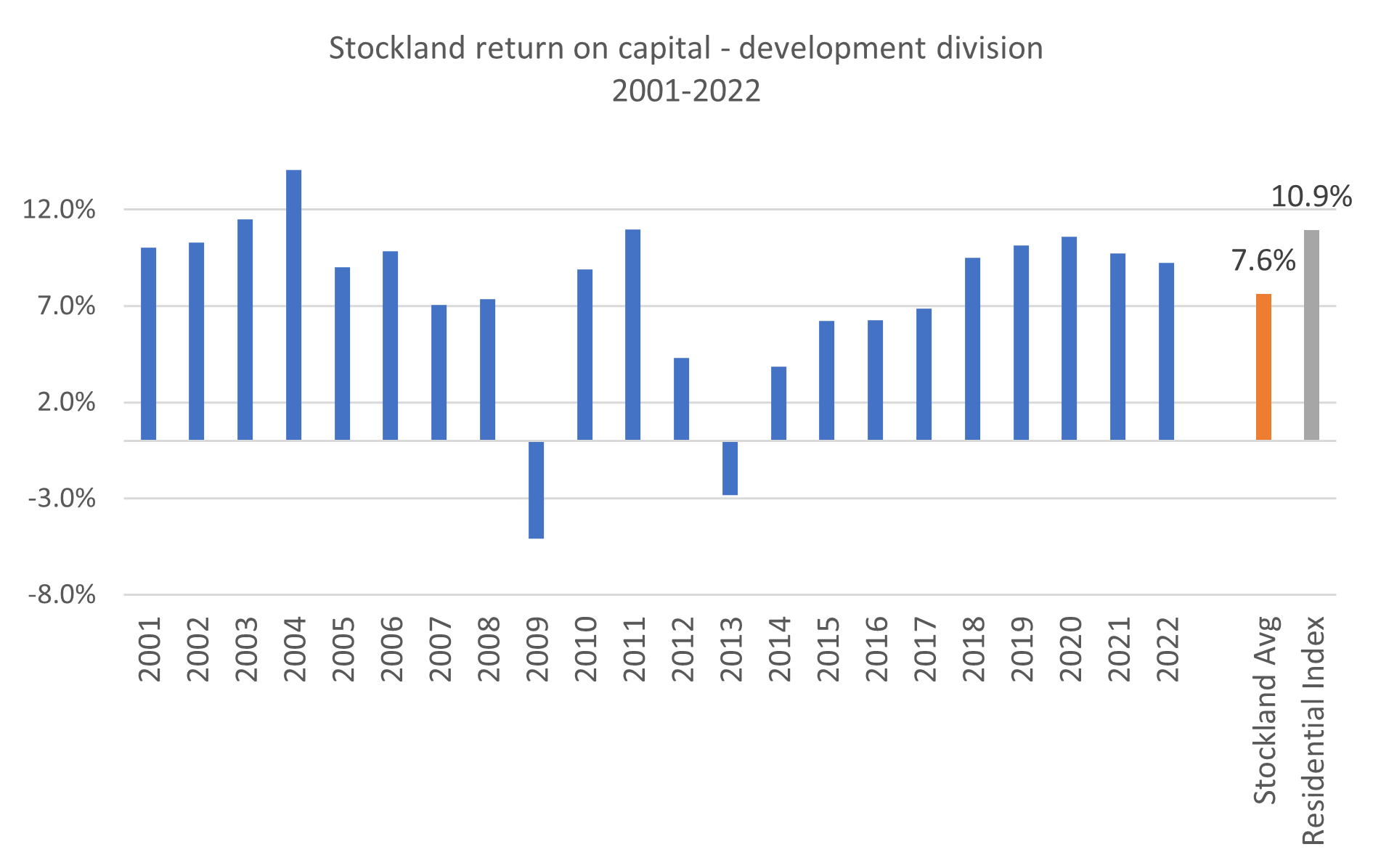

In an attempt to gain a clearer picture, we have analysed the historic segment reporting for both companies to look at the underlying profitability of the development businesses (based on return on average capital employed)[2]. We compare the average return on capital per annum to estimated total return (per annum) of the Australian housing market.

Source: Annual reports, ABS house price series, Quay Global Investors. Note Residential index assumes average 4% annual rental yield on initial purchase price.

Source: Annual reports, ABS house price series, Quay Global Investors. Note: Residential index assumes average 4% annual rental yield on initial purchase price.

Over the past 20 years, the average development returns on capital for Stockland (7.6%) and Mirvac (3.9%) have been poor to middling at best. Conversely, simply holding the passive unlevered asset would have provided a better total return of 10.9% per annum (including rent) with substantially lower risk.

What’s going on?

Contrary to some public commentary, the numbers certainly do not support the thesis of a ‘property bubble’ or greedy developers profiting from land banking at the expense of hard-working Australians.

Many of our readers are well aware of our views on the drivers of long-term property prices – while interest rates can affect short-term movement and sentiment (1-2 years), and a mismatch in demand and supply can affect medium-term movements (2-5 years), the long-term growth of property prices simply reflect the rising replacement costs.

Stockland and Mirvac bear the impost of ever-increasing replacement cost - year in, and year out. This not only includes the rising cost of labour and materials, but also the relentless increase in government rates, charges and taxes that all ultimately get baked into the final cost of production.

But these costs can simply be passed on in the end price. So, we believe there are other issues at play. Specifically:

- For developers, accounting profit can be very different to economic profit, resulting in poor capital allocation decisions

- In a rising cycle, developers are always restocking inventories at higher prices. And when the cycle turns, previous years’ reported profits are lost to subsequent write-down in inventories and work in progress.

The difference between accounting and economic profit

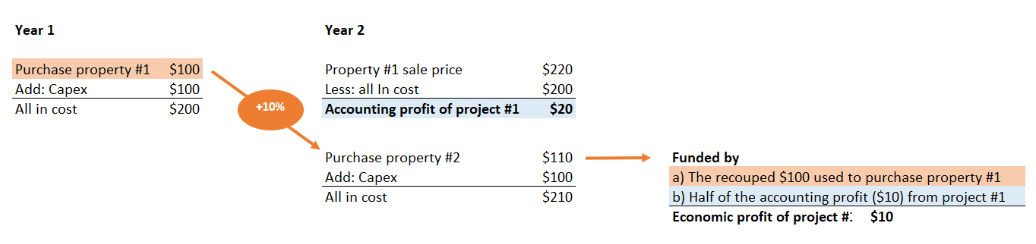

The development model is pretty simple: buy a property (or land), add capital and design, and sell it for more than the total cost of the project. Recycle capital (initial investment, CAPEX and profit) and do it all over again.

But upon sale, how much of the gain (accounting profit) is from value-add, and how much is simply from the cycle? If a developer simply buys a property for $100, adds $100 in CAPEX and sells in one year for $220, that represents $20 in profit, right? But what if the overall residential market rose 10% that year? It means it now costs the developer $110 to re-invest in a new site (or land).

So, to end up with the same starting inventory (one site), the developer has to invest $10 of the $20 along with the initial $100. So, while the accounting profit is $20, the economic profit was really only $10. This phenomenon is set out below.

Source: Quay Global Investors.

This mismatch between economic and accounting gain can lead to poor capital management decisions. To return $20 to shareholders in the form of a dividend really represents $10 of gain and $10 of return of capital (since the developer now needs to borrow the extra $10 for the new site acquisition). The ‘conservative payout ratios’ of 60-70% of accounting profit are not that conservative at all, which is why as the cycle ages, developers tend to take on more leverage.

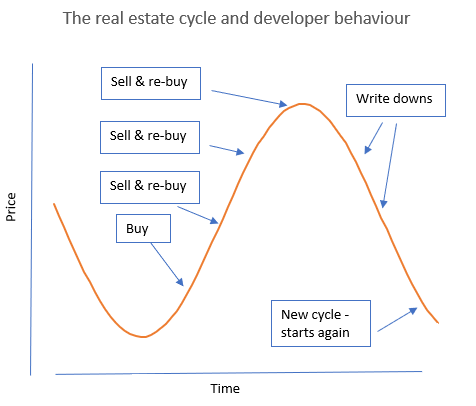

This leads to the second issue, restocking at the peak of a cycle.

The risks of restocking

One of the challenges of a listed developer is that no CEO or CFO wants to pitch to the board they want to shrink the business. Apart from anything else, it’s not a great look when trying to negotiate remuneration.

But that is precisely what a rational developer should do as the cycle matures. If not, they will simply get caught with too much inventory at the top of the cycle.

The diagram below demonstrates this point. As the developer recycles their capital into new projects during the up cycle, they are acquiring the same volume of inventory but at higher price. What makes it worse, is that during this period, CEOs and CFOs want to show growth – so the number of projects also must increase, so capital invested accelerates near the peak of the cycle. As the cycle turns, shareholders are faced with multiple years of write-downs, obliterating the equity.

Source: Quay Global Investors

The cycle is inevitable

The cornerstone philosophy at Quay is that prices (for most forms of real estate) oscillate around replacement cost. As prices rise above the cost to build, rational actors will enter the market and supply new stock. They will continue to do so until it is no longer profitable, usually when prices fall as a result of excess supply or some external shock.

This means that any business operating a development model faces an inevitable downturn, the timing of which can be extremely difficult, if not impossible to pick. For the CEO and CFO who are compensated for earnings growth, many companies are not even incentivized to look for the turning points.

It’s therefore not surprising that local developers are now turning to different operating models that have been proven to be successful overseas, such as build-to-rent and land-lease models. These models are able to generate more sustainable recurring income. The challenge, as always, will be to generate a sufficiently attractive return on capital to deliver adequate long-term shareholder returns.

How this impacts Quay’s investment approach

At Quay, we have always actively excluded property companies and REITs that rely on development profits as part of their business model from our investment universe. Not only does the data show the through-cycle returns on these businesses are challenged, but to sustain their business model, they also rely on real estate prices remaining above replacement cost. We prefer to acquire listed real estate below replacement cost for better risk adjusted returns. Thus, ownership of listed developers conflicts with this philosophy.

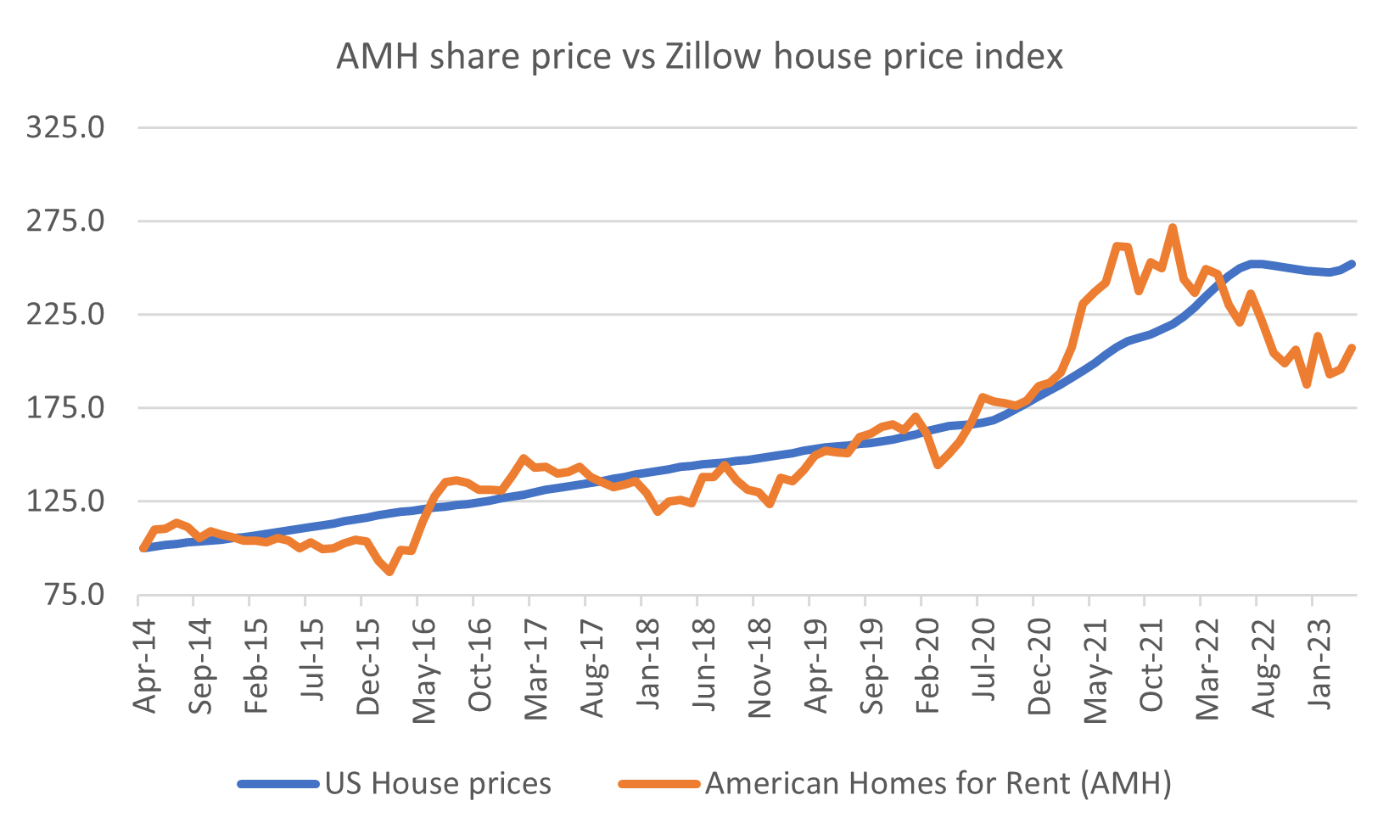

For investors who wish to participate in the emerging upswing in global residential prices, there are opportunities in listed REITS, with portfolios of already-built homes which listed price historically track the direct markets, yet in our estimation are currently trading below replacement cost. These are the opportunities that excite us the most, with one current example being American Homes for Rent (AMH).

Source: Zillow, Bloomberg, Quay Global Investors. Note: Zillow index adjusted for leverage consisted with AMH equity

It would be fair to say that this predictable and long-term approach is ‘boring’ compared to the excitement associated with a significant development project coming to life. However, at Quay we are not concerned with what is entertaining, we are purely focused on the preservation and creation of wealth for our investors across various market cycles.

[1] Calculated before non-cash gains and losses on asset values, inventories, and financial derivatives.

[2] For both companies, the development business (at times) includes commercial real estate and other businesses – however the majority of the development assets and income derived from residential activities

Author

| Name | Quay Global Investors |