ClearBridge 2023 Infrastructure Outlook

PUBLISHED

2023-01-18

Content

by Nick Langley, Charles Hamieh and Shane Hurst

Key Takeaways

- Secular growth drivers for infrastructure should be on full display in 2023, as the dire need for infrastructure spending underpins growth for the next decade, and the first steps for meeting long-term climate and electrification goals are being taken now.

- The second phase of bear markets is generally an earnings recession, and we expect that to be a force in 2023, albeit with a muted impact on infrastructure.

- Energy security, onshoring or reshoring, investments in wireless towers and industry-transformative tax credits in the U.S. Inflation Reduction Act driving renewables and utilities investments are among the tailwinds for infrastructure in 2023 and beyond.

To learn more about the global outlook for 2023, watch Portfolio Manager Nick Langley discuss longer-term thematics and their impact on global listed infrastructure.

Infrastructure Earnings Look Better Protected Compared with Global Equities

Like a stone tossed in a lake, the pandemic continues to create ripple effects across the global economy. From no growth in 2020 to rapid growth in 2021 to slow growth in 2022, we look at 2023 with a base case of recessions in the U.S., Europe, and the U.K. Growth in China should be below trend for at least a good portion of 2023. Bond yields should push higher heading into 2023 before abating alongside inflation later in the year.

For equities, the first part of this bear market has been characterized by contracting multiples driven by higher bond yields. The second phase of bear markets is generally an earnings recession, and we expect that to be a force, particularly in early 2023.

The impact on infrastructure, though, should be muted. Particularly for our regulated assets, where the companies generate their cash flows, earnings and dividends from their underlying asset bases, we expect those asset bases to increase over the next several years. As a result, infrastructure earnings look better protected compared with global equities.

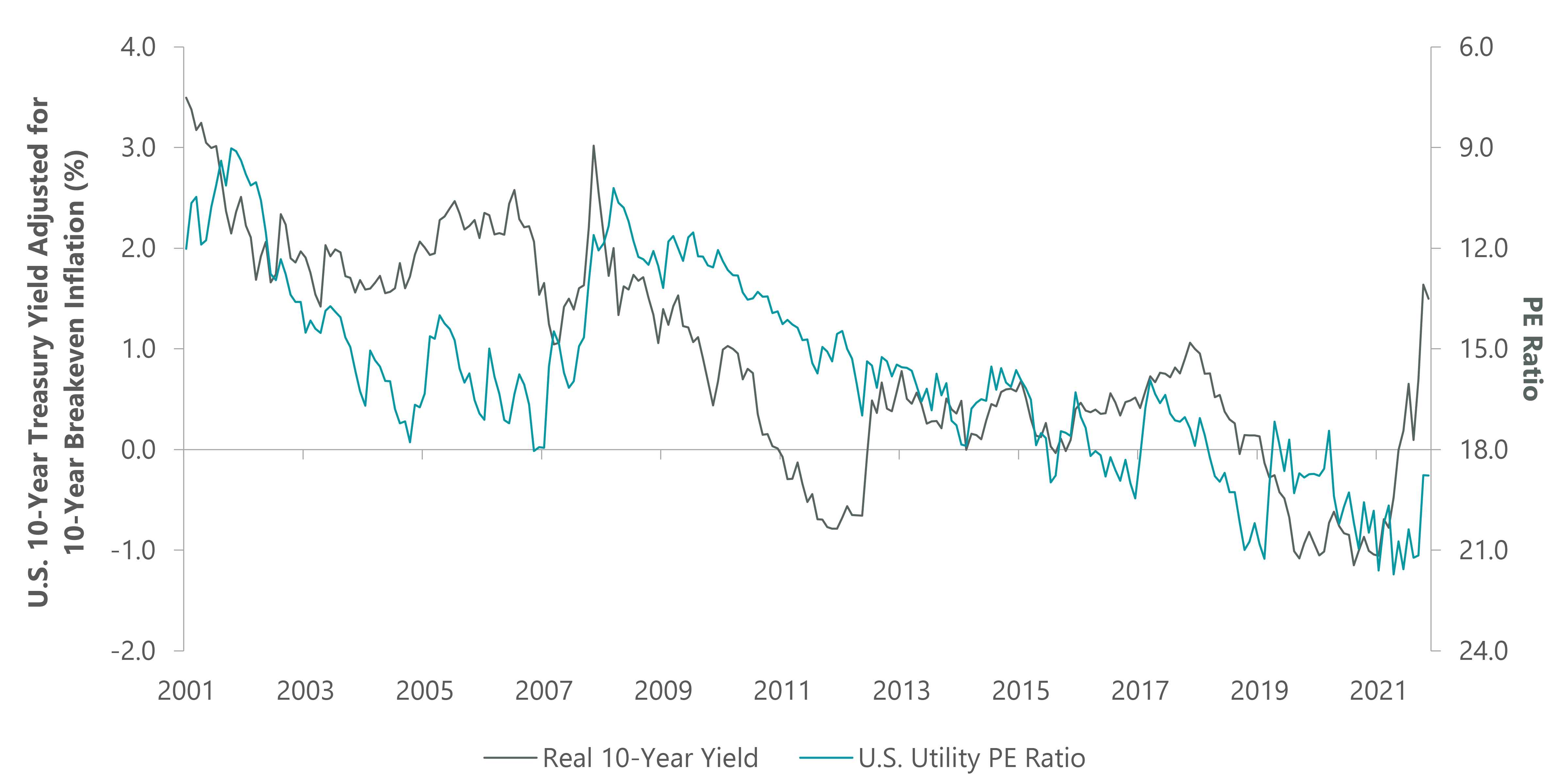

Most infrastructure companies have a link to inflation in their revenue or returns. Regulated assets, such as utilities, have their regulated allowed returns adjusted for changes in bond yields over time. As real yields rise, utilities look poised to perform well (Exhibit 1), and we have tilted our infrastructure portfolios to reflect this.

Exhibit 1: U.S. 10-Year Real Yield Versus Utilities P/E

As of Oct. 31, 2022. Source: ClearBridge Investments, Bloomberg Finance.

As a result, the underlying valuations of infrastructure assets are relatively unaffected by changes in inflation and bond yields. However, we have seen equity market volatility associated with higher bond yields impact the prices of listed infrastructure securities, making them more compelling when compared with unlisted infrastructure valuations in the private markets.

On top of its relative appeal versus equities, infrastructure should also benefit from several macro drivers in 2023 — and beyond. First, energy security is currently driving policy decisions, and a significant amount of infrastructure will need to be built for nations to obtain it. High gas prices and supply constraints brought on by the Russia/Ukraine war have highlighted the importance of energy security and energy investment. This is supportive of energy infrastructure, particularly in Europe, where additional capacity is needed to supplant Russian oil and gas supply, and in the U.S., where new basins are starting up, in part to meet fresh demand from Europe.

In transport, changing trade routes and adjustments to supply chains to bring production closer to home, either through reshoring or near-shoring, are driving demand for new transport infrastructure. Airports are still struggling to return to pre-pandemic passenger levels, which will likely be interrupted by a global recession in 2023, as well as changes in long-term trends like business travel. Communications infrastructure continues to roll out 5G, develop 6G technology and work to reduce network latency, driving significant investments in wireless tower businesses, generally undertaken under long-term inflation-linked contracts. Although, in the short term, higher interest costs are hitting the bottom line.

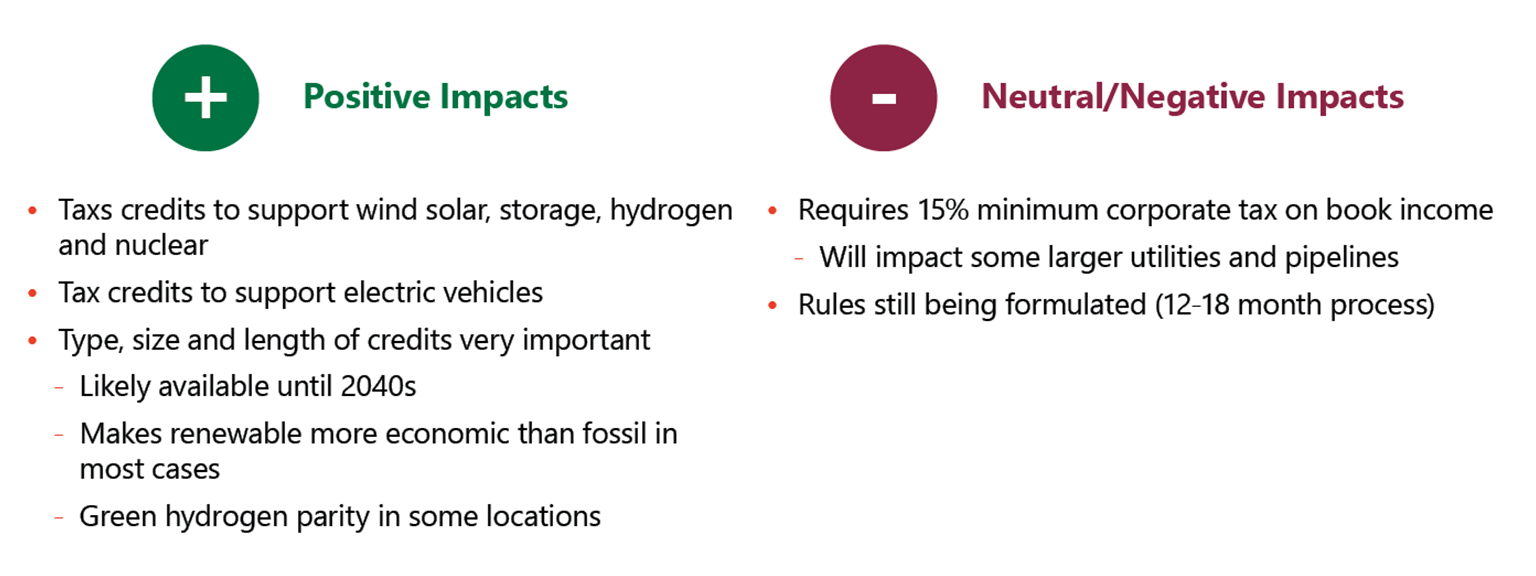

In terms of fiscal policy, the U.S. Inflation Reduction Act (IRA), signed into law in August 2022, is the most significant climate legislation in U.S. history. We believe it will be industry transformative (Exhibit 2) for utilities and renewables in particular. The growing need for electrification — more electric vehicle charging infrastructure, more residential and small commercial rooftop solar — will require new substations, new transformers and upgraded wires along distribution networks. We already see its impact in the 2023 capital expenditure plans of utilities, together with the forward order books of companies involved in the energy transition, such as renewable, storage and component suppliers, increasing their growth profile.

Exhibit 2: Inflation Reduction Act: Key Impacts

Source: ClearBridge Investments.

One major macro takeaway from the IRA: there is no reason to build anything other than renewables from now on. Much of this is due to tax credits. Production tax credits for solar/wind are available until 2032 or until a 75% reduction in greenhouse gases is achieved (based off 2022 numbers). Either way, this is expected to be a tailwind for investment for well over a decade.

Secular growth drivers for infrastructure should be on full display in 2023. President Biden wants to reduce emissions in the U.S. by 50% by 2030, with roughly half of U.S. power coming from solar plants by 2050. It will require nearly $320 billion to be invested in electricity transmission infrastructure by 2030 to meet net zero by 2050. This dire need for infrastructure spending underpins growth for the next decade and beyond, and the first steps for meeting these long-term goals are being taken now.

Explore The ClearBridge RARE Infrastructure Income Fund - Hedged.