The Most Anticipated Recession Ever

PUBLISHED

2023-01-13

Content

by Jeffrey Schulze and Josh Jamner

Key Takeaways

- With a deep red signal emanating from the ClearBridge Recession Risk Dashboard and a Fed clearly willing to tolerate economic pain in order to restore price stability, we believe a recession is likely in 2023.

- While this view is aligned with consensus, there is less agreement on the timing and depth of a potential recession. The Fed remains focused on lagging indicators, which risks a delayed and more modest policy response if a recession occurs. This could result in a longer and deeper downturn relative to the short and shallow recession expected.

- We believe earnings present the greatest risk to 2023 as the second phase of the bear market plays out, following the first phase driven by multiple compression. However, the ultimate impact for equities could be softer than earnings revisions suggest given market losses to date.

Timing and Depth of Expected Recession Still Up for Debate

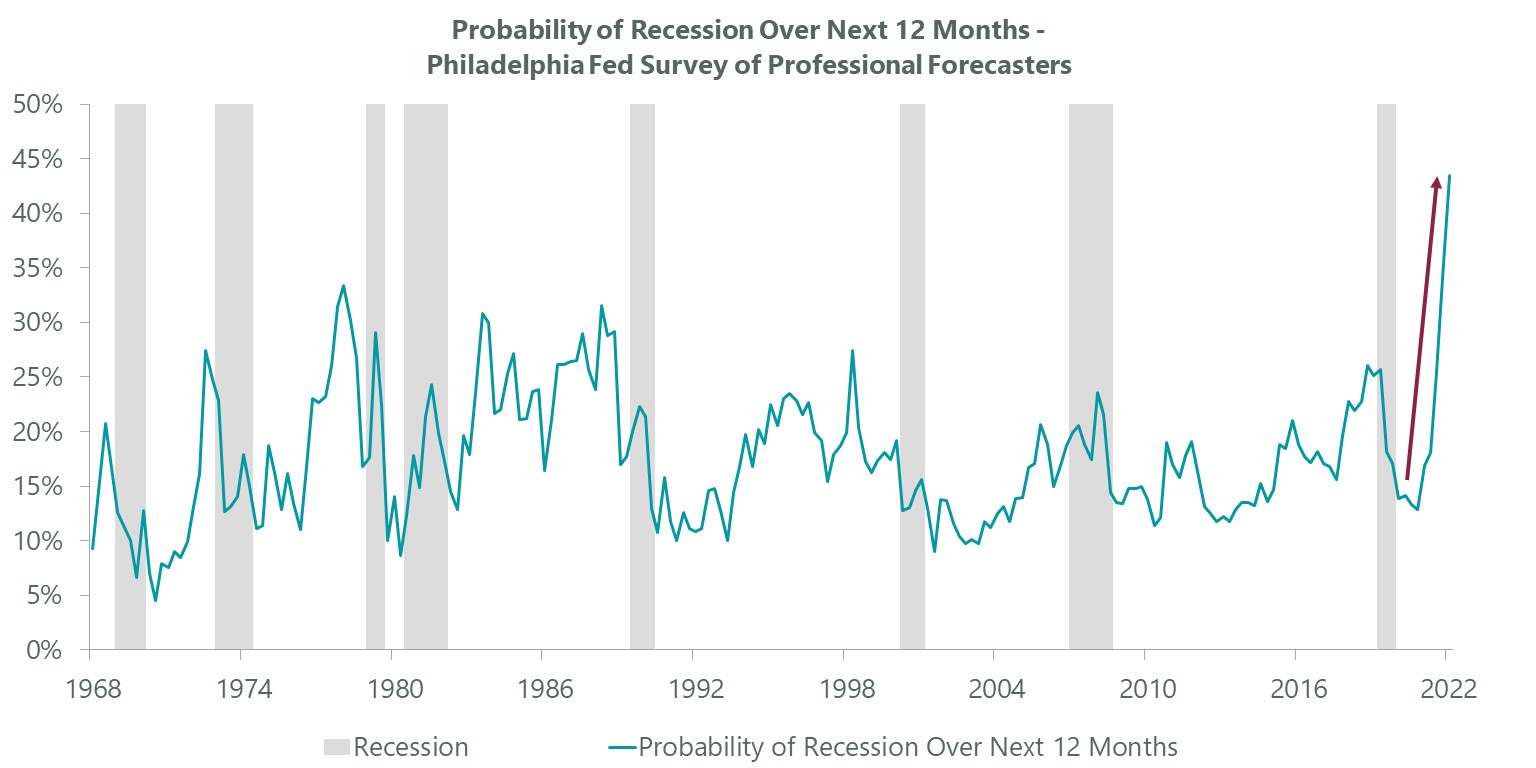

The changing of the calendar is a natural time to reflect on the past year as well as envisage the future. A year ago, few thought inflation would near double-digit territory or that the Federal Reserve would embark upon the most rapid monetary tightening in four decades. Forecasting the future is inherently challenging if not impossible. As a result, it is natural to question whether the consensus view for a recession in the coming year will come to fruition. With the Philadelphia Fed Survey of Professional Forecasters showing the highest probability of a recession over the next 12 months in the survey’s 55-year history, many are asking: “If everyone believes a recession is coming, could it become a self-fulfilling prophecy?”Exhibit 1: Most Anticipated Recession Ever

Data as of Dec. 31, 2022. Source: Federal Reserve Bank of Philadelphia, FactSet.

The answer could be yes, particularly if businesses curb investment in anticipation of weaker demand or consumers pull back on spending in expectation of tougher times ahead. However, it isn’t as simple as that. Recessions are typically driven by the unwinding of excesses that have built up in the economy, meaning that a potential downturn could be more limited in scope if such excesses do not yet exist. Furthermore, if some excesses do not build — for example, banks have already tightened lending standards — then the consensus view for a recession could prove self-inhibiting rather than self-fulfilling.

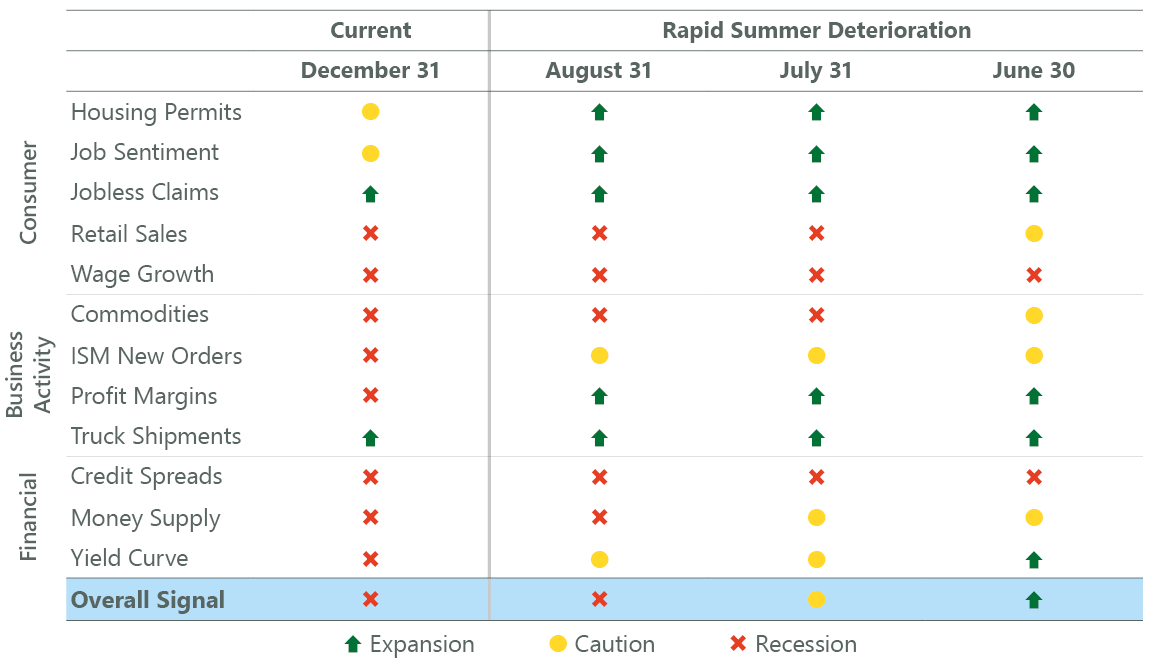

It’s tempting to fall back on longtime Merrill Lynch strategist Bob Farrell’s ninth rule of investing: when all the experts and forecasts agree, something else is going to happen. However, consensus is often right if unglamorous, and given the determination from the Fed to restore price stability and the deep red recessionary signal emanating from the ClearBridge Recession Risk Dashboard, we find our views aligned with consensus in believing the economy is more likely than not to roll over in 2023. A recession has been our base case since mid-June when we published a special update and our conviction in this view has been hardened in the months since, given the degradation of the dashboard and an unwavering Fed. There were no signal changes for the dashboard last month.

Exhibit 2: ClearBridge Recession Risk Dashboard

Data as of Dec. 31, 2022. Source: BLS, Federal Reserve, Census Bureau, ISM, BEA, American Chemistry Council, American Trucking Association, Conference Board, and Bloomberg. The ClearBridge Recession Risk Dashboard was created in January 2016. References to the signals it would have sent in the years prior to January 2016 are based on how the underlying data was reflected in the component indicators at the time.

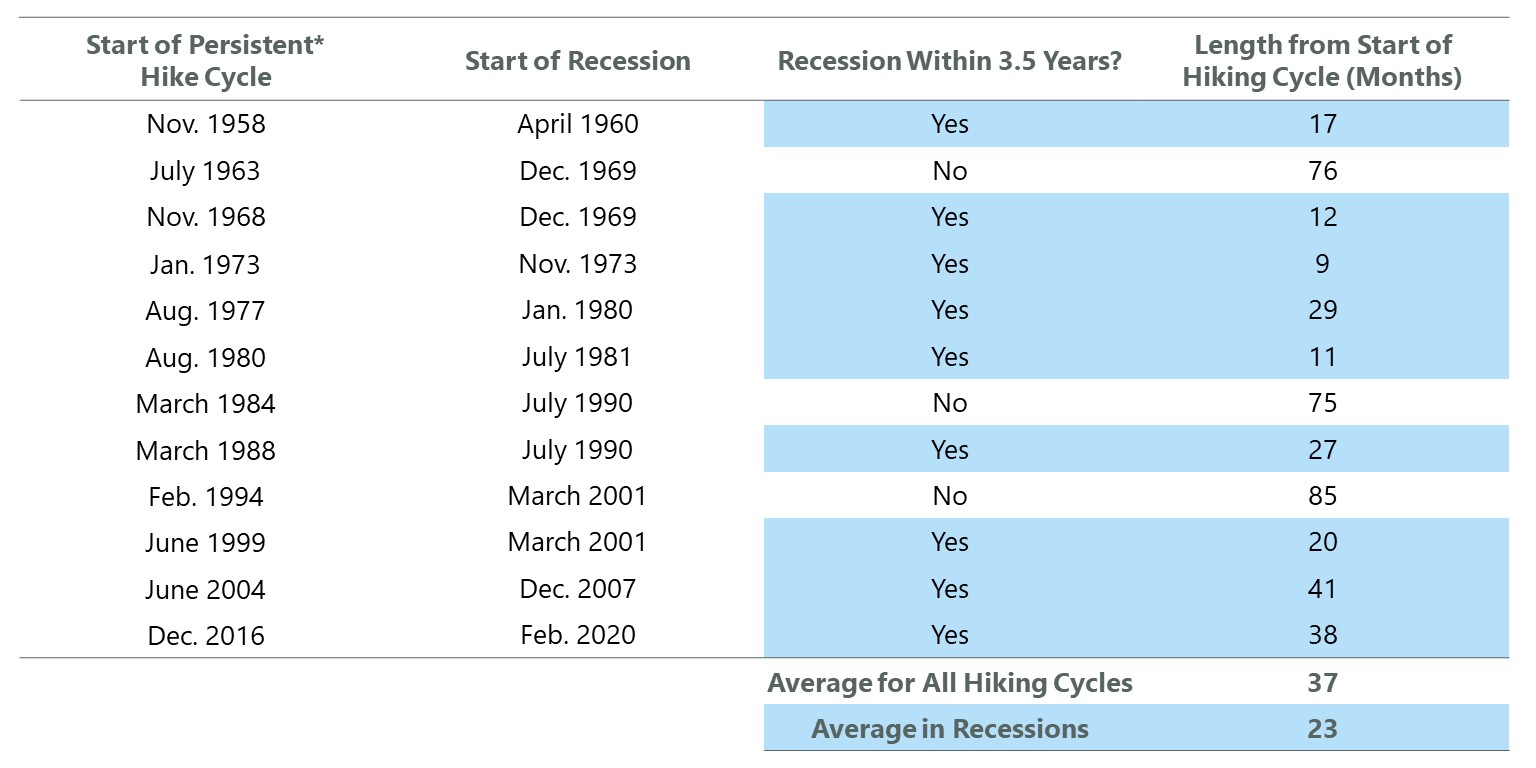

Although a recession is widely expected, there is less agreement regarding its potential timing and depth. One way to gauge timing can be to look at the Fed and how long an economic expansion typically continues once the central bank begins to tighten policy. Historically, a recession has begun around two years after the start of a hiking cycle — particularly those that were implemented later in an economic expansion. While it may feel like a lifetime ago, the Fed began hiking only nine months ago. Although the shortest gap between the start of tightening and a recession is nine months (1973), history suggests the long and variable lags with which monetary policy acts will push off the start of a recession several quarters.

Exhibit 3: Long and Variable Lags

*Persistent Hike Cycle is when the vast majority of Fed rate hikes in a tightening cycle occur and may not align with initial hike when there have been long delays between initial and subsequent hikes. Source: FactSet.

Many believe a recession would likely be shallow given fewer excesses have built up during the current expansion. The banking system, consumers and corporations all appear to be heading into a possible downturn with strong balance sheets, which could limit downside. However, the Fed may have less flexibility with which to operate if the recession proves quite mild initially and inflation stays high. The potential lack of a large jump-start from monetary policy to end the recession is amplified by a Fed keen to avoid repeating the mistakes of the past. In the late 1960s, the central bank prematurely eased policy (pivoted), setting off a longer inflationary cycle that required further and more severe pain to correct later on, which we discussed in last quarter's Long View.

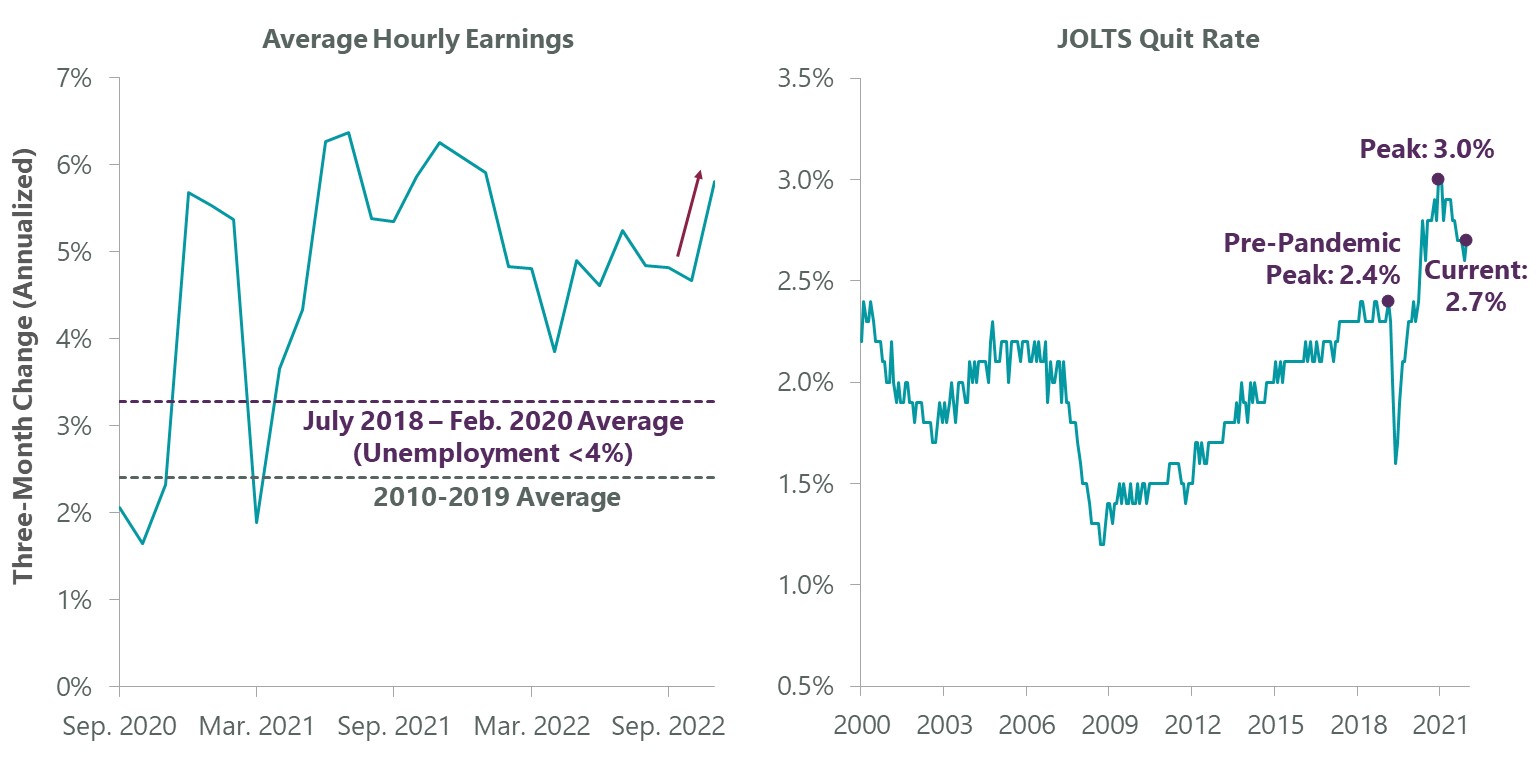

Two primary metrics the Fed uses are lagging in nature, which intensifies risks that it may end up overtightening, given worries of easing too early. In fact, wages (unit labor costs) and service sector inflation are two components of the Conference Board’s Lagging Economic Index®, which focuses on datapoints that typically follow the cycle and often peak well after a recession has already begun. These areas may not ease in the near future given the significant cost of living adjustments (COLA) many workers have been pushing for and receiving recently. Employer leverage to resist these requests is currently thin given the tight labor market with the quits rate still higher than anything seen in the two decades pre-pandemic.

Exhibit 4: Workers Have the Upper Hand

Data as of Nov. 30, 2022, latest available as of Dec. 31, 2022. Source: FactSet, U.S. Department of Labor.

The Fed has been clear that wage gains are currently running too hot for inflation to return to 2%, which in part drove the shift in their latest “dots” toward an even higher expected policy rate (5.1% from 4.6%) in 2023 along with a larger pickup in the unemployment rate (4.6% from 4.4%).

This is notable because never in modern history has the unemployment rate risen 0.5% from year-earlier levels without the U.S. either having already fallen into recession or having been on the cusp of one. This is known as the Sahm Rule, and highlights both the lagging nature of the labor market as well as Newton’s first law: objects in motion tend to stay in motion. Historically, the unemployment rate has risen by at least 2.2% in cycles associated with recessions, and the average increase has been 4.1%.

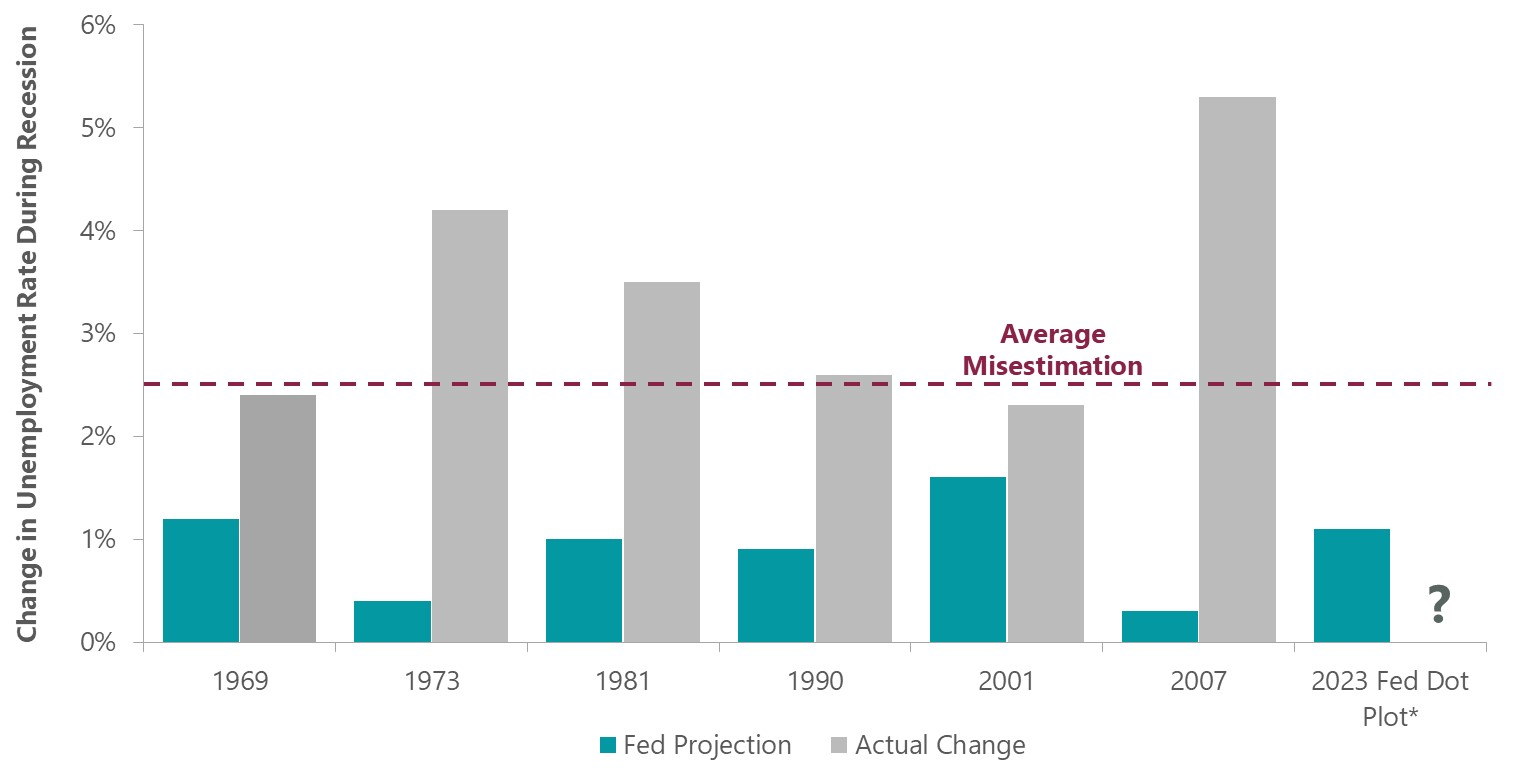

Although the Fed is optimistic that robust job openings currently means there is room to soften the labor market and cool wages with fewer actual jobs being lost, history suggests the Fed has rose-colored glasses with regard to potential labor market weakness heading into recessions. Specifically, Fed forecasts have underestimated the rise in unemployment by 2.5% on average. If this holds, unemployment could rise above 7% in the coming potential downturn, which is hardly consistent with a shallow recession.

Exhibit 5: The Fed’s Rose-Colored Glasses

*2023 Fed Dot Plot is for a 4.6% unemployment rate vs. a recent low of 3.5%. Data as of Dec. 31, 2022. Source: FactSet, Philadelphia Fed Tealbook database, Federal Reserve Bank of St. Louis.

How much of the potential downturn is already priced in? This is a fair question to ask with the S&P 500 Index down over 20% from its early January 2022 peak and a recession widely anticipated. Historically, the market has not fully priced a recession until one becomes abundantly clear. The key signal appears to have typically come from the labor market, with a negative non-farm payroll reading required for the market to reassess what might be coming. Although payroll gains have slowed from their red-hot pace in late 2021 and early 2022, they are still nowhere near negative territory. In fact, job creation over the past few months is still running at a pace more than 50% above the gains experienced late last cycle when the unemployment rate fell below 4%, a level considered maximum employment.

Beyond the labor market, the health of corporate earnings are vital to the path forward for equities. In July’s Long View, we highlighted the two typical phases of a bear market: 1) multiple compression, and 2) falling earnings expectations. Lower P/E ratios were the primary driver of market weakness in 2022 as earnings revisions have held up reasonably well, with next-12-month expectations down only 4.1% from their peak in July. During the last three recessions, next-12-month earnings expectations fell by 25.8% on average, and we believe earnings present the greatest risk in 2023 as the second phase of a typical bear market potentially plays out.

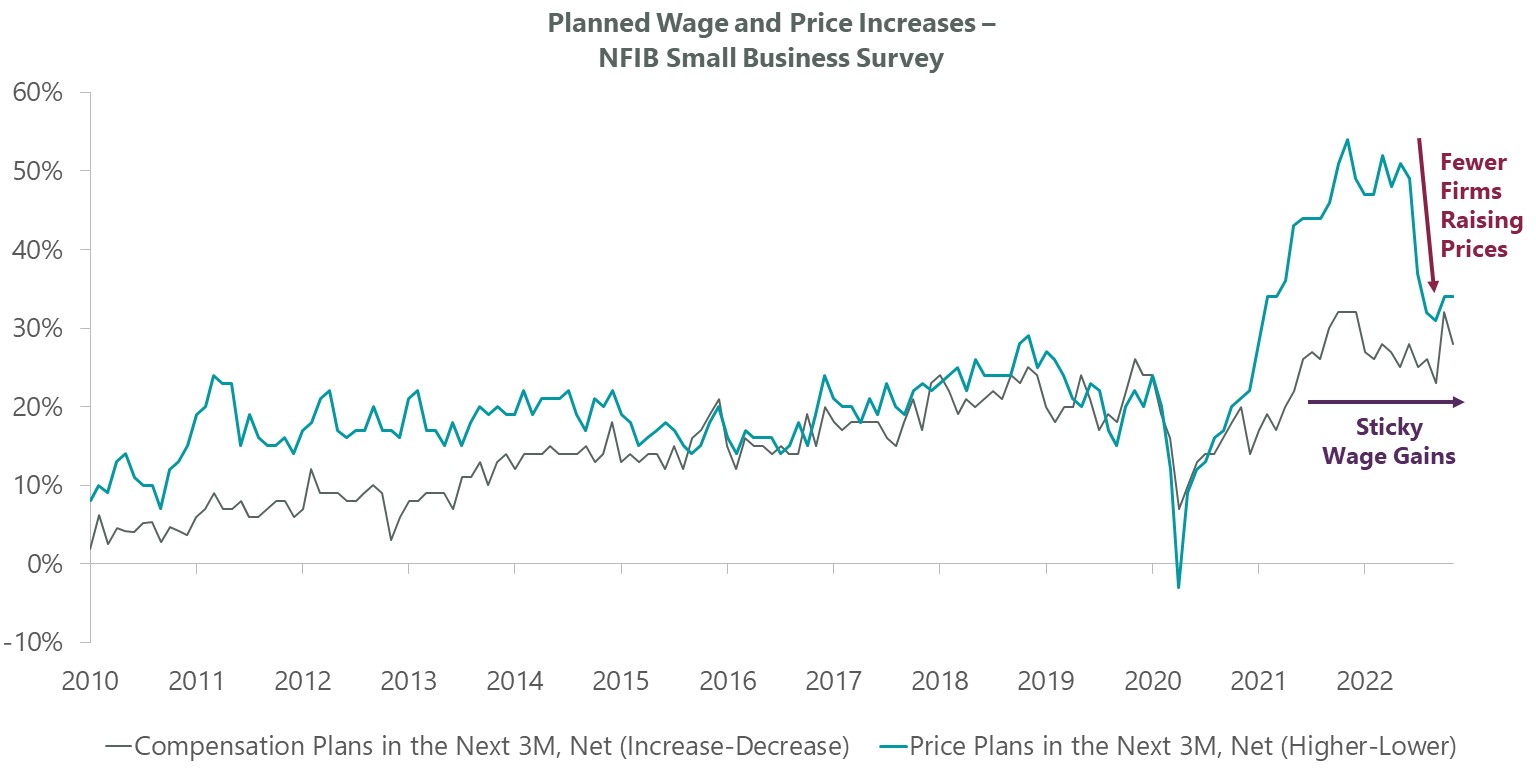

The coming reporting season could prove to be a make-or-break moment for this thesis, with many companies needing to update guidance for 2023. Earnings seem likely to come under pressure from a combination of slowing top-line growth as the economy decelerates and shrinking margins as wage gains remain sticky. This dynamic has shown up in the NFIB Small Business Survey, which shows a rapidly declining share of small businesses planning to increase prices in the coming three months, while the percentage planning to raise wages is holding mostly steady.

Exhibit 6: Small Business Pain Ahead

Data as of Nov. 30, 2022, latest available as of Dec. 31, 2022. Source: FactSet, NFIB.

This is an important reversal from the end of the pandemic, when expectations for both growing prices and wages were becoming more pervasive and price gains were outpacing wages, leading to margin expansion. The shifting landscape is not specific to small businesses, and if it persists, will likely lead to further cost-cutting measures, including reductions in capex and even layoffs.

Bear Markets are Long-Term Buying Opportunities

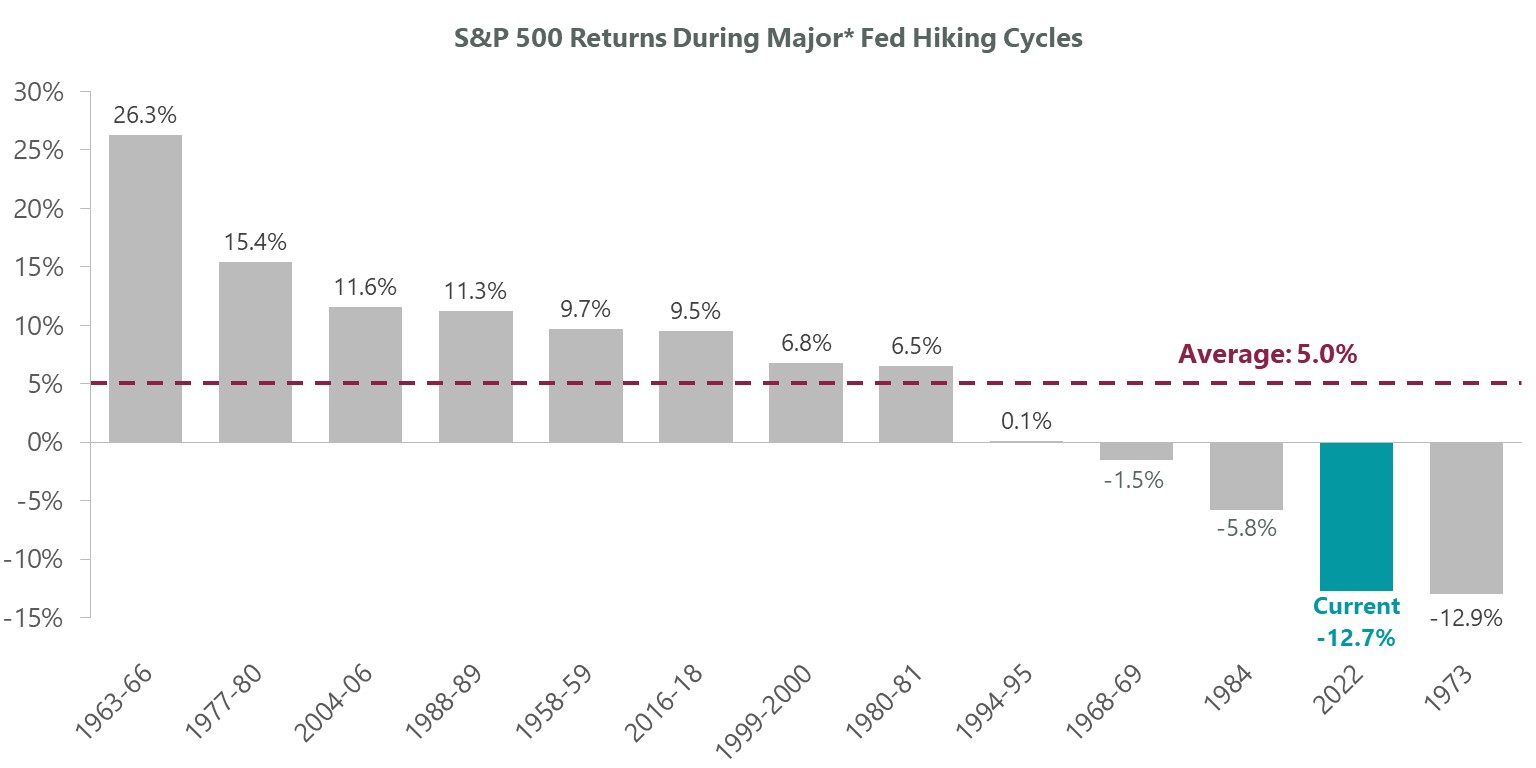

Although earnings appear to be at risk, the outlook is not all bad for equity investors. Little about the last three years can be described as “typical,” and the market may have priced in more of the downside at this point than usual. Specifically, in the 12 major hiking cycles since the mid/late 1950s, the S&P 500 has experienced a positive return 75% of the time, delivering an average gain of 5%. The current hiking cycle so far is only one of two, along with 1973, where markets suffered double-digit losses, meaning the blow from here could be softer as the path for monetary policy, the economy and earnings becomes clear.Exhibit 7: A Particularly Tough Cycle

*Major Hiking Cycles are when the vast majority of Fed rate hikes in a tightening cycle occur, and may not align with initial hike when there have been long delays between initial and subsequent hikes. Source: FactSet.

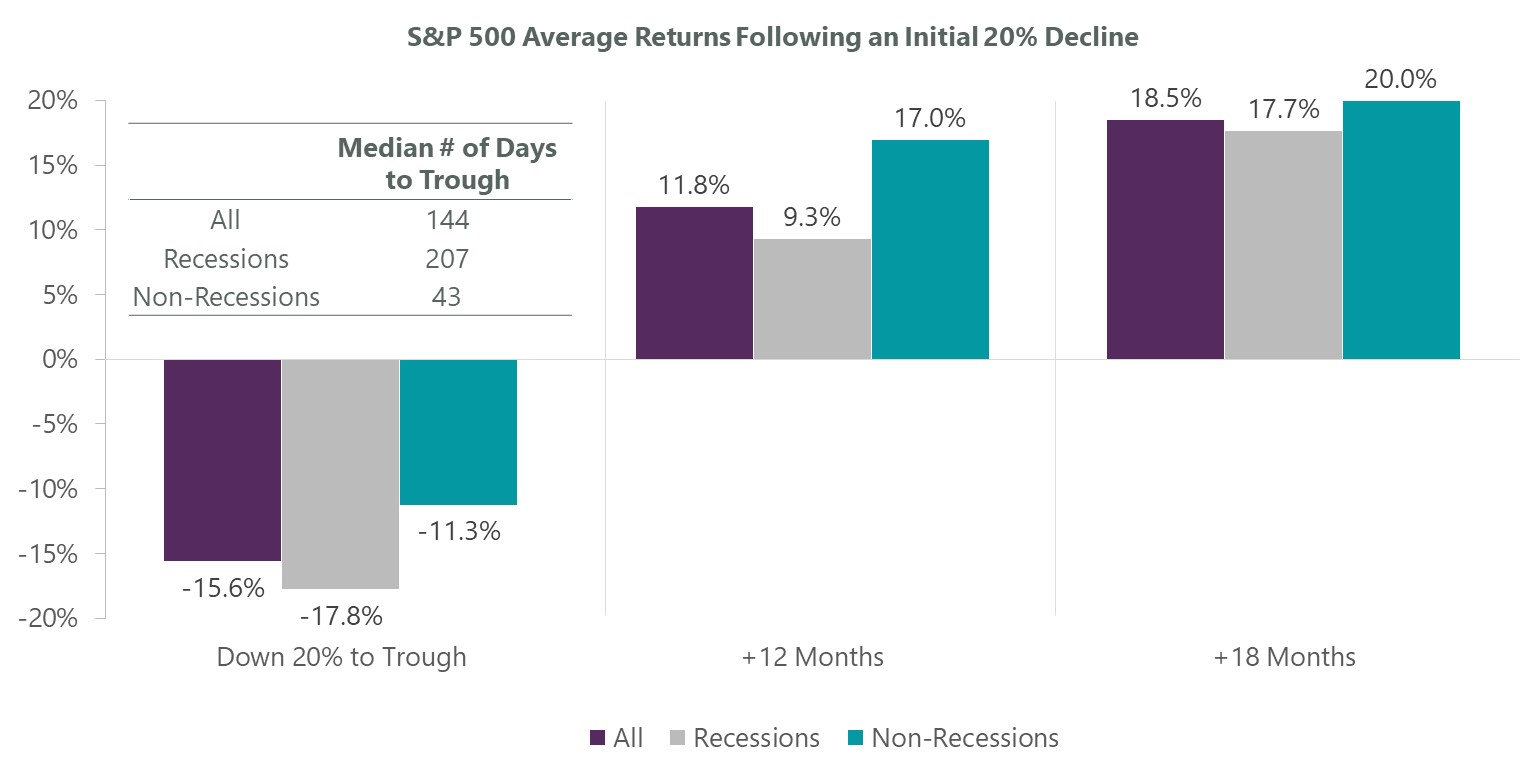

Markets may retest or even break through the October lows in 2023, but we believe long-term investors can benefit from deploying capital methodically and opportunistically into equities. Over the last 80 years, equities have fallen an additional -15.6% on average after breaching the -20% bear market threshold. However, long-term investors may want to take advantage of selloffs of such magnitude, with the additional losses once in bear market territory typically quickly recovered. On average, the market has rallied +11.8% in the year after bear market territory was reached (and +18.5% over the subsequent 18-month period), inclusive of subsequent losses. With the S&P 500 bear market threshold having officially been breached over six months ago, history suggests investors may turn out to be pleasantly surprised in 2023.

Exhibit 8: Bear Market Achieved, Good Entry Point?

Source: S&P, Factset, and NBER.

There are plenty of reasons why the economy could remain resilient in the near term. Firms are still hiring at a robust pace, wage gains remain elevated, consumer spending is holding up, and Congress recently passed a $1.7 trillion spending bill. Combined, these factors should provide an economic boost that forestalls an imminent recession. However, robust economic growth is a double-edged sword, as it could encourage the Fed to keep policy restrictive if inflation cools more than expected or the labor market holds up better than anticipated.

In times of transition, it’s paramount to adhere to the old adage: “Don’t Fight the Fed.” While Powell & Co. could end up pivoting sooner than they are currently telegraphing, most signs point to the Fed employing “higher for longer” monetary policy due to the risk of structurally higher inflation. Although fewer excesses favor a shallower recession, a restrained central bank risks a deeper recession once one emerges. While longer-term investors have typically been well-compensated for adding risk at this point in past bear markets, we see a choppy first half of the year as the market tries to assess the ultimate direction for the economy and earnings while incoming data fails to reveal a clear trend. Consequently, we continue to favor higher quality and more defensive areas.